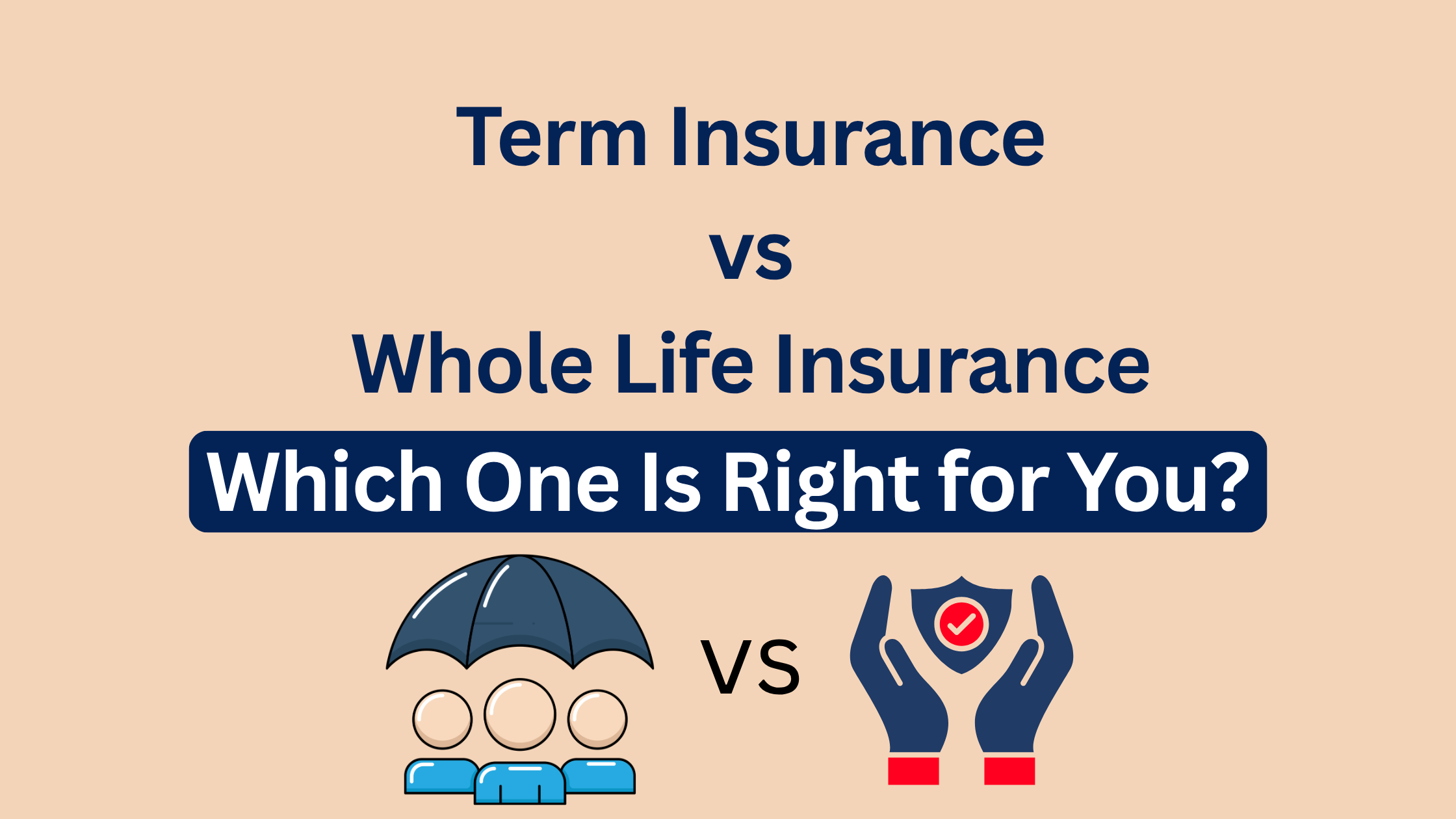

Insurance plays a crucial role in financial planning, especially when it comes to protecting your family’s future. Among the many types of life insurance policies available, Term Insurance and Whole Life Insurance are two of the most popular options. However, many people often get confused about which one is better and which policy suits their financial goals. Understanding the differences between these two types of insurance can help you make a smarter and more secure financial decision.

What Is Term Insurance?

Term insurance is a type of life insurance policy that provides coverage for a specific period or “term,” such as 10, 20, or 30 years. If the policyholder passes away during this period, the insurance company pays the sum assured to the nominee or beneficiary. However, if the policyholder survives the policy term, no maturity benefit is usually provided.

One of the biggest advantages of term insurance is that it offers high coverage at an affordable premium. Because it focuses purely on protection and does not include an investment component, the premiums are generally much lower compared to other life insurance policies. This makes term insurance an excellent option for young professionals, individuals with financial dependants, or anyone looking for maximum financial protection at a lower cost.

Another important feature is flexibility. Policyholders can choose riders such as critical illness cover, accidental death benefit, or disability cover to enhance the protection offered by the policy.

What Is Whole Life Insurance?

Whole life insurance, as the name suggests, provides coverage for the entire lifetime of the policyholder, typically up to 99 or 100 years of age. Unlike term insurance, whole life policies often include a savings or investment component, which allows the policy to accumulate cash value over time.

The cash value component grows gradually and can sometimes be borrowed against or withdrawn, depending on the policy terms. This feature makes whole life insurance not only a protection plan but also a long-term financial asset.

Another benefit of whole life insurance is that it guarantees a death benefit to the nominee regardless of when the policyholder passes away, as long as the premiums are paid regularly. This makes it a suitable option for individuals who want lifelong coverage and a financial legacy for their family.

However, these benefits come at a cost. Premiums for whole life insurance are significantly higher compared to term insurance because the policy combines insurance protection with a savings element.

Major Differences Between Term Insurance and Whole Life Insurance

Understanding the differences between these two policies can help you decide which one suits your needs.

Coverage Period

Term insurance provides coverage for a fixed period such as 10, 20, or 30 years. This type of insurance provides permanent coverage that continues throughout the insured person’s life.

Premium Cost

Term insurance premiums are generally low and affordable. Whole life insurance premiums are higher because the policy includes both protection and savings components.

Investment Component

Term insurance focuses purely on financial protection and does not accumulate cash value. Whole life insurance includes a savings element that builds cash value over time.

Maturity Benefits

In most cases, term insurance does not provide any maturity benefit if the insured survives the policy period. Whole life insurance may offer cash value accumulation and sometimes bonuses.

Purpose

Term insurance is ideal for income replacement and financial protection for dependants. Whole life insurance is more suitable for long-term financial planning, wealth transfer, and legacy creation.

Advantages of Term Insurance

Term insurance is often considered the most straightforward and cost-effective life insurance option. One of its biggest advantages is affordability, which allows policyholders to get a high coverage amount for a relatively small premium.

It is also easy to understand because it focuses purely on financial protection. If the policyholder dies during the policy term, the family receives the sum assured. This can help cover living expenses, loan repayments, children’s education, and other financial needs.

Another benefit is flexibility in choosing the coverage duration based on your financial responsibilities, such as the years until retirement or until your children become financially independent.

Advantages of Whole Life Insurance

Whole life insurance provides lifelong coverage, which ensures that your family will receive financial support whenever the policyholder passes away. This guarantee can provide peace of mind for individuals who want long-term security for their loved ones.

The policy also builds cash value over time, which can serve as a financial asset. Some people use this cash value for emergencies, loans, or even retirement planning.

Additionally, whole life insurance can be useful for estate planning and wealth transfer, ensuring that future generations receive financial support.

Which Insurance Is Better?

The answer depends largely on your financial goals, budget, and personal circumstances.

If your primary goal is to secure your family financially at an affordable cost, term insurance is often the better option. It allows you to get a large coverage amount without putting too much pressure on your monthly budget.

On the other hand, if you are looking for lifelong protection along with a savings component and are comfortable paying higher premiums, whole life insurance might be a suitable choice.

Financial experts often suggest that young individuals with limited budgets should start with term insurance because it provides strong financial protection during their most financially vulnerable years.

Conclusion

Both term insurance and whole life insurance play important roles in financial planning. Term insurance is simple, affordable, and focused purely on protection, making it ideal for individuals who want maximum coverage at a lower cost. Whole life insurance, on the other hand, provides lifelong protection along with a savings component that can help build long-term financial security.

Before choosing a policy, it is important to evaluate your financial responsibilities, long-term goals, and budget. By understanding the differences between term insurance and whole life insurance, you can select the policy that best protects your family and supports your financial future.

A well-planned insurance strategy not only safeguards your loved ones but also gives you peace of mind knowing that their future will remain secure even in your absence.